November CPI Cools to 2.7% — But Can the Fed Trust It? Government Shutdown Distortion and January 2026 Rate Cut Expectations

November CPI slowed to 2.7%, but government shutdown distortions raise doubts. Here’s how markets price January 2026 Fed rate cut odds.

Key Takeaways

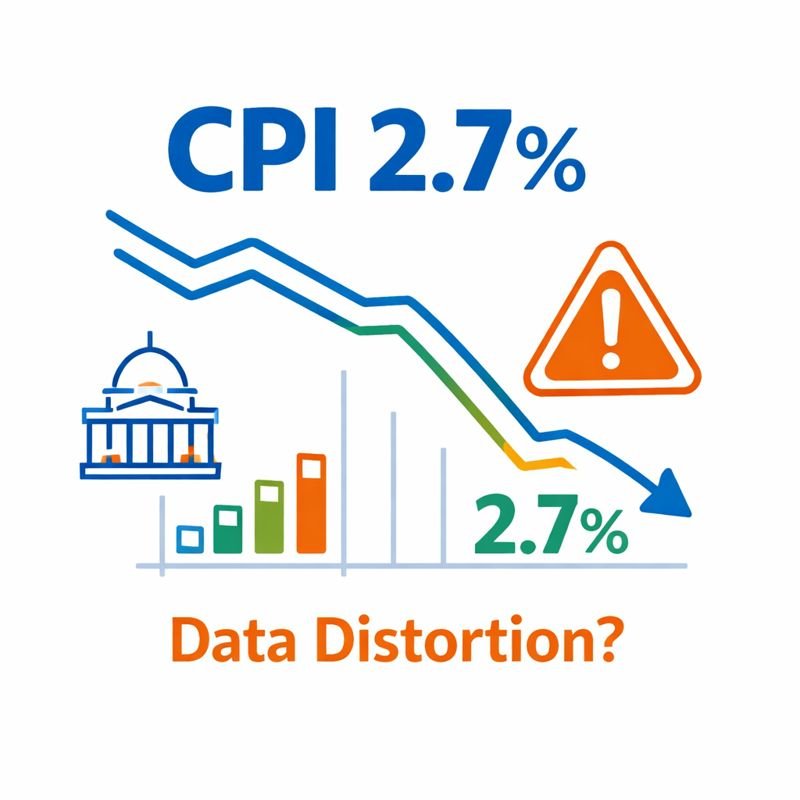

✔ November CPI fell to 2.7% YoY, with core CPI at 2.6%.

✔ The data is clouded by a federal government shutdown that disrupted October price collection.

✔ The BLS confirmed CPI data collection resumed on November 14, 2025.

✔ Markets price a January 2026 rate cut at roughly 25–30%, with a hold still the base case.

The November Consumer Price Index (CPI) initially looked like welcome news. Inflation cooled faster than expected, easing fears that price pressures were re-accelerating. Markets reacted quickly, with Treasury yields falling and risk assets stabilizing.

However, this CPI report comes with an important caveat. The 2025 federal government shutdown disrupted the CPI data collection process, raising questions about how reliable the latest inflation signal really is.

This article explains why November CPI should be interpreted cautiously and how investors should think about January 2026 Fed rate cut expectations through the lens of data quality, not just headline numbers.

Why the November CPI Number Moved Markets

At face value, the November CPI report suggested inflation is moving closer to the Fed’s comfort zone. Both headline and core readings softened, reinforcing the narrative that disinflation is back on track.

This was enough to spark short-term optimism. Lower inflation reduces pressure on the Fed to keep policy restrictive and supports equity valuations, especially for rate-sensitive sectors.

How the Government Shutdown Affected CPI Data

The problem lies beneath the surface. According to the Bureau of Labor Statistics (BLS), price collection for October CPI was not conducted during the shutdown and could not be retroactively recovered.

CPI data collection only resumed on November 14, 2025, meaning the November reading was calculated without a complete and continuous monthly survey framework. This breaks the normal month-to-month comparison that CPI relies on.

Timing Matters: CPI Collection vs. Discount Season

The timing of the data restart matters even more. CPI collection resumed during peak discount season, including Black Friday and early holiday promotions.

This raises the risk that temporary price discounts were over-represented, making inflation appear cooler than the underlying trend. While some components can be adjusted using alternative data, overall basket representativeness may still be compromised.

November CPI Interpretation Checklist

|

Factor |

What We Know |

Why It Matters |

|---|---|---|

|

Inflation level |

CPI 2.7%, Core 2.6% |

Supports disinflation narrative |

|

Data continuity |

October survey missing |

Trend reliability weakened |

|

Seasonal bias |

Heavy discount overlap |

Potential underestimation |

|

Policy impact |

Fed favors consistent data |

One report is not decisive |

January 2026 Rate Cut Expectations: Reading the Probabilities

According to the CME FedWatch Tool, markets currently assign a 25–30% probability to a rate cut at the January 2026 FOMC meeting.

This does not signal confidence in an imminent easing cycle. Instead, it reflects optionality. Investors acknowledge the possibility of a cut, but still expect the Fed to wait for confirmation from additional data, especially December CPI released in January.

November CPI at 2.7% is encouraging, but the real issue is data reliability, not inflation alone. Until the Fed sees consistent, shutdown-free inflation readings, January 2026 rate cut expectations will remain conditional rather than certain.

References

- BLS CPI News Release (November 2025)

- BLS | Impact of the 2025 Federal Government Shutdown on CPI

- Reuters | US Inflation Moderates in November Amid Data Gaps

- Wall Street Journal | Inflation Eased to 2.7% in Report Distorted by Shutdown

- CME Group | FedWatch Tool